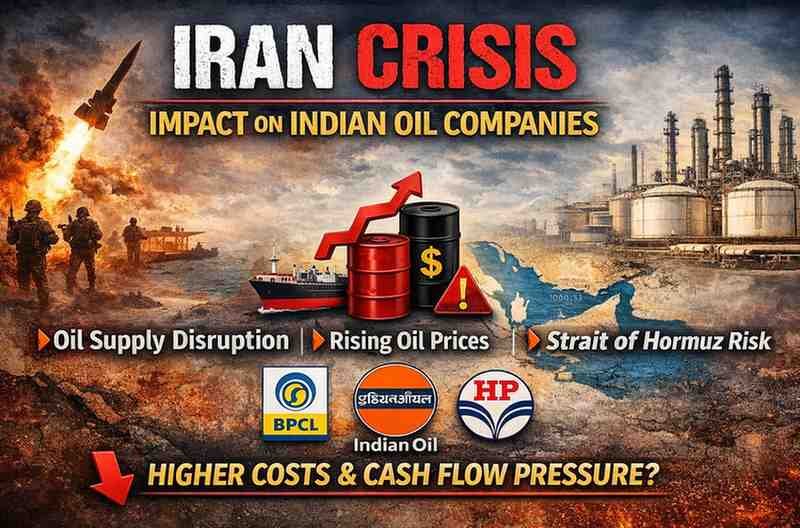

Iran Crisis Impact on Indian Oil Companies

If the Iran crisis continues for a long time, pressure on Indian oil companies may increase. High oil prices could impact cash flow.

According to Fitch Ratings if the oil supply disruptions caused by tensions with Iran persist for a prolonged period, cash flow pressure could increase on Indian oil marketing companies and GAIL India Limited. According to the report, if the Strait of Hormuz remains closed or oil prices remain high for a prolonged period, these companies’ financial indicators could be impacted.

However, ratings of state-owned companies are expected to be supported by strong government support.

According to Fitch, among the rated OMCs, Bharat Petroleum Corporation Limited (BPCL) has the strongest balance sheet buffers to deal with prolonged supply disruptions or higher crude oil prices, followed by Indian Oil Corporation Limited and Hindustan Petroleum Corporation Limited.

Fitch stated that the government will likely maintain a balance between oil companies’ financial health and inflation control, as has been observed in previous periods of crude oil price volatility. According to the report, GAIL’s leverage could increase if LNG supplies from the Middle East are disrupted. However, due to its lower dependence on imported feedstock and stronger balance sheet, it may be less affected by long-term supply disruptions than rated OMCs.

India imports nearly half of its natural gas needs, and approximately 60 percent of LNG supplies from the Middle East. If LNG from the Middle East is not available for one quarter, GAIL’s EBITDA net leverage could reach approximately 2.5 times in the fiscal year ending March 2027, compared to the previously estimated 1.8 times. If supply disruptions persist for two quarters, this leverage could reach nearly 3 times. This could be impacted by weak petrochemical earnings, reduced LNG marketing and transmission volumes, and increased working capital requirements.

Companies may try to mitigate the impact by reducing LNG use in petrochemicals, purchasing spot cargoes, and slowing capital expenditure. According to Fitch, if Brent crude prices reach around $90 per barrel for a quarter due to the Iran-related disruption, OMCs’ EBITDA net leverage could increase by approximately 0.4 to 0.6 times in FY27. In such a scenario, refining margins could double, while marketing profits could fall to zero.

Companies can manage short-

term volatility through balance sheet capacity, but prolonged pressure could impact cash flow and credit buffers. According to Fitch, standalone refiners like Reliance Industries could also face mixed impacts from higher crude oil prices. They may initially benefit from inventory gains and stronger product margins, but if supply constraints persist, there could be a risk of crude oil shortages and to maintain refinery operational.